Abstract

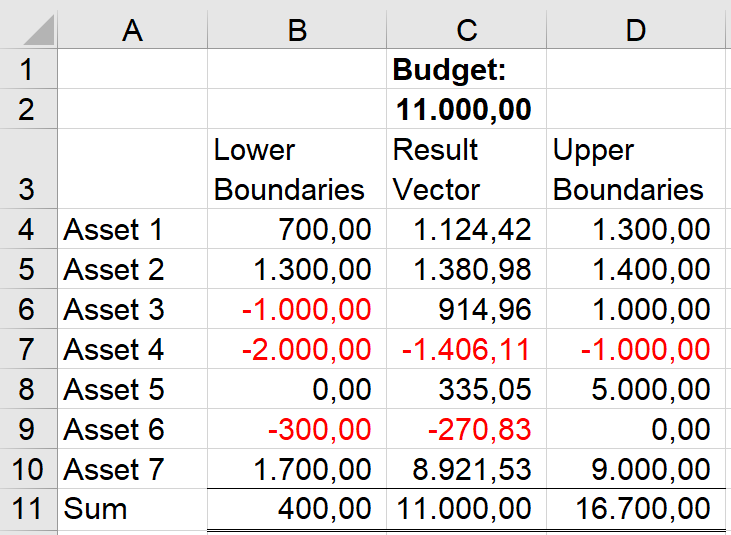

If you need to generate random portfolios with a given total sum and lower boundaries and upper boundaries for each asset, you can take the function PF_Allocate() shown below.

Appendix – PF_Allocate Code

Please note that this program needs (calls) VBUniqRandInt.

Please read my Disclaimer.

Option Explicit

Function PF_Allocate(db As Double, _

vlb As Variant, _

vub As Variant) As Double()

'Generate a portfolio of assets x1..xN

'x1..xN being random numbers (double) with:

'x1+x2+..xN = db 'budget

'xi >= vlb(i) 'lower bound vector

'xi <= vub(i) 'upper bound vector

'Reverse(moc.liborplus.www) V0.11

'Source (EN): http://www.sulprobil.com/pf_allocate_en/

'Source (DE): http://www.bplumhoff.de/pf_allocate_de/

'(C) (P) by Bernd Plumhoff 26-Jul-2020 PB V0.11

Dim i As Variant, n As Long

Dim dcumx As Double

Dim dcumlb As Double

Dim dcumub As Double

Dim dxlb As Double

Dim dxub As Double

'Application.Volatile

dcumlb = Application.WorksheetFunction.Sum(vlb)

dcumub = Application.WorksheetFunction.Sum(vub)

If dcumlb > db Or dcumub < db Then

PF_Allocate = CVErr(xlErrValue)

Exit Function

End If

n = vlb.Count

ReDim dR(1 To n) As Double

dcumx = 0#

'For i = 1 To n 'Old biased solution

For Each i In VBUniqRandInt(n, n)

'Source (EN): http://www.sulprobil.com/uniqrandint_en/

If vlb(i) > vub(i) Then

PF_Allocate = CVErr(xlErrValue)

Exit Function

End If

dcumlb = dcumlb - vlb(i)

dcumub = dcumub - vub(i)

dxlb = db - dcumx - dcumub

If dxlb < vlb(i) Then dxlb = vlb(i) 'dxlb = Min(..)

dxub = db - dcumx - dcumlb

If dxub > vub(i) Then dxub = vub(i) 'dxub = Max(..)

dR(i) = dxlb + Rnd() * (dxub - dxlb)

dcumx = dcumx + dR(i)

Next i

PF_Allocate = dR

End Function

Download

Please read my Disclaimer.

PF_Allocate.xlsm [24 KB Excel file, open and use at your own risk]